Hall Capital “Market Views” Newsletter October 2018

This is the 34th edition of Market Views from HALL CAPITAL. Our aim is to provide concise views of where we see risk and opportunity for investors.

Trade Drives Global Growth

- and always will

Global economic growth is highly dependent on the expansion of $15 trillion in global trade annually. The US exports $2.2T in goods and services and imports $2.7T for a net deficit of some $500B. I have contended that the tariffs so far have not been significant enough to derail the economy. Prices are going up for some goods, but the real risk is a meaningful reduction in trade due either due to price or to supply chains disruptions.

Much has been made of the US/China trade deficit. All agree that China needs to honor IP, but that is a different issue the trade deficit. The WTO is a set of rules and a court. This is where members bring grievances on trade offenses. This court has served our interests well with the US winning over 90% of the cases it has brought before the court. Yet President Trump has denounced the WTO as not fair to the US. (He also pulled out of the Trans Pacific Partnership but modified our trade relationship with Mexico with a few changes mostly called for by the TPP!)

Chinese workers work for less and save more. That "offense" will certainly boost their trade surplus. US politicians complain that this has cost American jobs. It has indeed, but far less than automation. The jobs that Americans wish they had back are not sewing eyes on teddy bears but the highly paid ones, like steel manufacturing. China supplies very little steel to the US. The main sector driving the US trade deficit with China is electronics.

The American work force is fully employed today, though many are in low paying jobs. Chinese workers assemble an iPhone for $18. I strongly doubt bringing iPhone assembly back to the US would increase wages or job satisfaction over, say, being a barista at Starbucks or a driver for Uber.

All this is to say that much of the bluster on trade is misguided and pursued due to political messaging value. It's like a game of chicken. We are driving a big SUV and our trading partners are driving a sedan. We have the advantage. But a collision can still hurt. Fortunately, more than elected politicians are at the wheel and understand that we all win if trade expands -- fairly of course.

PS: As I was about to send out this letter it appears that the US may have reached a constructive agreement with Canada. Some of the updates, like Mexico, include modernization aspects included in the original TPP.

Bonds Don't Have More Fun

- and won't for a long time

Our first letter over 8 years ago noted our preference for stocks over bonds. Interest rates have declined mostly for 35 years until 2017. Fun times for bond investors over the next several years will be few and far between. Recently bonds have been dealing with several challenges which are on-going: (1) A strong US economy,(2) Related to this: low unemployment which is driving wages higher,(3) Aforementioned tariffs driving up costs on some goods, (4) Higher oil prices, and finally (5) A Federal Reserve raising short rates.

This is not to say that bonds don't have some role in a portfolio as they are the best hedge against recession risk -- it's always nice to have something to sell during a recession to buy bargain stocks. The main problem is the low return even after the recent rise in rates. The 10 year UST bond is yielding 3% which is less than 1% after inflation. This return is not very interesting, especially given the risk that some day the US may monetize its $21 Trillion debt driving inflation higher than 3%.

Rising rates can be a challenge for stocks too, but stocks can benefit from some of the factors that are driving bond prices down. Wages bending up sharply could take its toll on both stocks and bonds, but that development may have other positive elements.

Focus List Surges 16%

- doubling the S&P 500 return

The Focus List returned 15.9% in Q3 compared to a 7.7% return for the S&P 500. Even laggard CVS outperformed, rebounding 23% for the period.

We contend the out-performance of the FL was accomplished without taking more risk than the market. The FL is a conservative list of "stalwarts". This is not to say that the surge in the prices of our stocks will not correct to some degree. But the earnings outlook for each holding on the FL is positive, but not explosive. .

Driven mainly by stalwarts, since inception over eight years ago, the Focus List has averaged a compounded annual return of 17.8% vs 15.8% for the S&P 500.

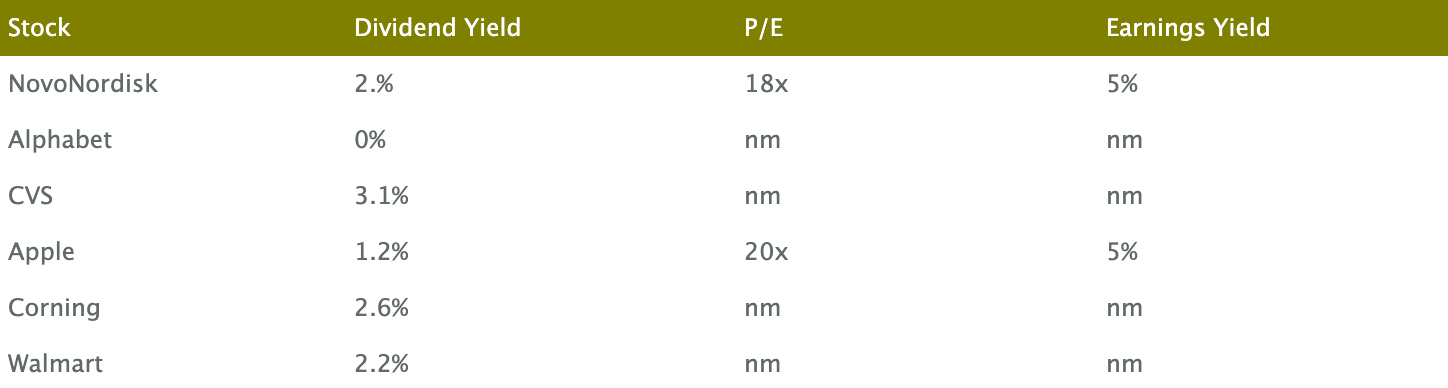

Some of the data below is shown as Not Meaningful due to the one time distortions due to the new tax law.

For individual stocks as well as selection strategies, past performance is not necessarily indicative of the future.

Hall Capital Focus List

Follow Up – from our letter one year ago

"The global economy is moving in the right direction currently. There are no conditions present which portend a recession. Thus, we remain tilted toward equities with some hedges."

- The global economy expanded over the last year and US stocks were up 18%.

"In due course volatility will return. It takes a recession to take the market down 25% to 35%. But a 5% to 10% correction could come at any time for no particular reason other than upsetting complacency."

- Four months later volatility spiked and the S&P 500 sold off by 10% in two weeks.

"Alphabet's (Google) dominant position and considerable human capital give it a greater chance to take advantage of advancing technology rather than falling victim to it."

- Alphabet is up 24% over the last year and remains in a dominate competitive position.

NOTE: Now in addition to ALL our quarterly letters, on our website is a tab with just the Follow Ups.

About HALL CAPITAL

HALL CAPITAL, LLC is a registered investment advisor and was formed by Principals from Arcturus Capital in 2010.

For more information, contact Donald Hall 626 578 5700 x101 dhall@hallcapitalmanagement.com

HALL CAPITAL | 199 S. Los Robles Ave | Suite 535 | Pasadena | CA | 91101