Hall Capital “Market Views” Newsletter April 2016

This is the 24th edition of Market Views from HALL CAPITAL. Our aim is to provide concise views of where we see risk and opportunity for investors.

Market Psychology Rules

- in the short term

This quarter's market action was like a jet hitting a down draft at 30,000 feet falling immediately 3,200 feet before resuming its altitude. That proportion of a decline is exactly what the S&P 500 did for the first five weeks of the year before gaining back all the altitude it had lost. With the benefit of hindsight it seems to have been mostly psychological, rather than fundamental.

Investors got focused on oil prices which were dropping precipitously. The stock market and oil prices seemed to be in lock step. Our view was the oil price collapse had more to do with an increase in supply than the lack of demand (though, granted, demand was not strong).

Then why did investors freak out?

Once stock prices headed down which could have been triggered by the selling by sovereign funds of oil dependent countries in need of more cash flow, worries began to crop up: will failures in the oil patch cause a contagion of bank failures? The experience of the mortgage crisis of 2008 seared investors so badly that any resemblance of a financial crisis brings bad memories to fore and investors run for cover.

We would argue that while we WILL see significant failures in the oil patch, this is NOTHING like the mortgage crisis. In 2008 banks had major exposure to mortgages and, therefore, to home values as did every American home owner. Energy is a big part of the economy, but no more than 20%. When energy prices go down, 80% of the economy benefits! Only a handful of credit default traders who had "the big short" benefited from the collapse of the US housing market. Look at it this way, oil prices declined by some two thirds. Do you think investors would feel better had oil tripled?

We have concerns, but low oil prices are not one. If you can determine that the market psychology is focused on one variable (wrongly) then that is usually an opportunity to take a position in the other direction.

Growth Continues Scarce

- as is income

We expect global slow growth to continue. This is not a bad environment for stocks, but hardly ebullient either. Our tilt remains in favor of equities but with some dry powder.

Those looking for low risk high income streams are out of luck. Japanese and European interest rates have gone negative. US money market rates are nil and 10 year US Treasuries are paying less than 2%.

High yield bonds sold off sharply last year and now appear to offer interesting value with many instruments yielding around 9%. That is, even with an average default rate, high yield bonds are competitive with stock returns and arguably with less risk considering the high reinvestment opportunity. The instrument choice for high yield is important. "Index" funds of the high yield sector are NOT attractive. This is a sector where active management clearly pays off. We prefer closed end funds or business development corporations trading at a discount.

Municipal bonds have value but plain vanilla quality taxable bonds, though not risky, simply don't offer an interesting return opportunity against a field of generally modest return alternatives.

Focus List Proves More Than Sturdy

- earning 8.4% in the quarter

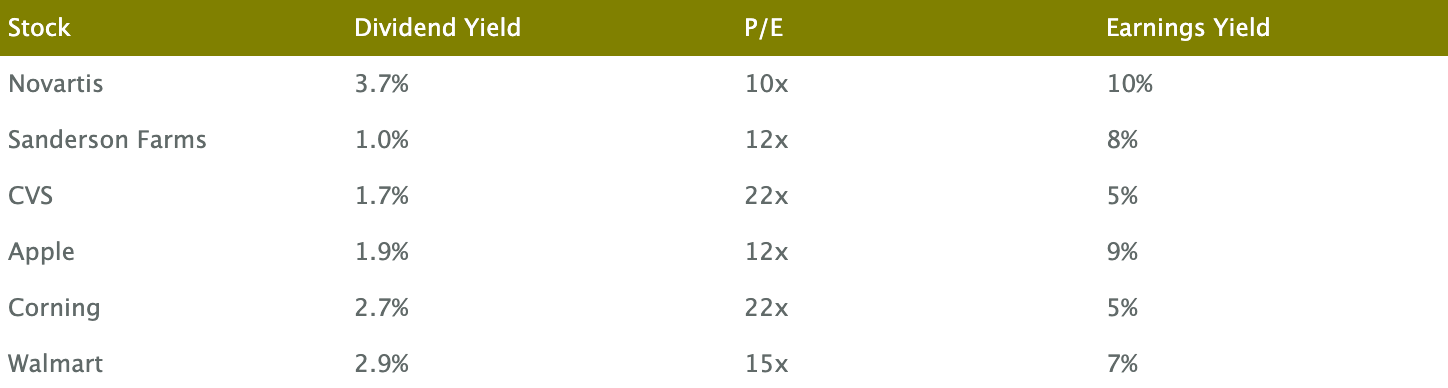

In a period that tested the market, all our Focus List stocks powered ahead but AmTrust Financial which we are dropping in favor of Novartis. AmTrust seems undervalued at 9x but we now question whether they have booked sufficient reserves. Novartis, the pharmaceutical giant, is higher quality and selling at only 10x with a generous 3.7% dividend yield.

The Focus List has doubled in the last five years earning an average annual return of 15.2%. This compares very favorably to the 11.6% return for the S&P 500. The S&P 500 was a particularly challenging benchmark over the last several years. Most equity mutual funds have lagged well behind this index.

Clearly, 8.4% for one quarter, which was 7% ahead of the 1.4% S&P 500 return is unusual, both relatively and absolutely. We would not expect this to occur often. Our goal has been simply to match the market without taking the same risk, by avoiding overly levered companies for example. Sometimes there is a bonus.

For individual stocks as well as selection strategies, past performance is not necessarily indicative of the future.

Hall Capital Focus List

Follow Up – from our letter one year ago

"Investment environment not inhospitable - but higher prices will limit gains"

- Indeed. Low growth without inflation continued, but stock prices did not advance over the last year. Only the dividend contributed to return.

"Alternatives are, well, an alternative with double digit expected returns"

- The primary one we used, which was a real estate debt fund, earned 10% over the last year.

"We have maintained that the Fed is NOT behind the curve on raising rates and has the luxury to not raise them in June as many expect."

- The Federal Reserve did not raise rates in June nor September, but waited til December for the first increase. We continue to believe that the Fed is not behind the curve and will only very slowly raise interest rates.

NOTE: Now in addition to ALL our quarterly letters, on our website is a tab with just the Follow Ups.

About HALL CAPITAL

HALL CAPITAL, LLC is a registered investment advisor and was formed by Principals from Arcturus Capital in 2010.

For more information, contact Donald Hall 626 578 5700 x101 dhall@hallcapitalmanagement.com

HALL CAPITAL | 199 S. Los Robles Ave | Suite 535 | Pasadena | CA | 91101